Steven R. Dunbar

Department of Mathematics

203 Avery Hall

University of Nebraska-Lincoln

Lincoln, NE 68588-0130

http://www.math.unl.edu

Voice: 402-472-3731

Fax: 402-472-8466

Math 489/Math 889

Stochastic Processes and

Advanced Mathematical Finance

Dunbar, Fall 2009

__________________________________________________________________________

Solution of the Black-Scholes Equation

_______________________________________________________________________

Note: To read these pages properly, you will need the latest version of the Mozilla Firefox browser, with the STIX fonts installed. In a few sections, you will also need the latest Java plug-in, and JavaScript must be enabled. If you use a browser other than Firefox, you should be able to access the pages and run the applets. However, mathematical expressions will probably not display correctly. Firefox is currently the only browser that supports all of the open standards.

_______________________________________________________________________________________________

Mathematically Mature: may contain mathematics beyond calculus with proofs.

_______________________________________________________________________________________________

What is the solution method for the Cauchy-Euler type of ordinary differential equation:

_______________________________________________________________________________________________

__________________________________________________________________________

__________________________________________________________________________

We have to start somewhere, and to avoid the problem of deriving everything back to calculus, we will assert that the initial value problem for the heat equation on the real line is well-posed. That is, consider the solution to the partial differential equation

We will take the initial condition

We will assume the initial condition and the solution satisfy the following technical requirements:

Under these mild assumptions, the solution exists for all time and is unique. Most importantly, the solution is represented as

Remark. This solution can derived in several different ways, the easiest way is to use Fourier transforms. The derivation of this solution representation is standard in any course or book on partial differential equations.

Remark. Mathematically, the conditions above are unnecessarily restrictive, and can be considerably weakened. However, they will be more than sufficient for all practical situations we encounter in mathematical finance.

Remark. The use of for the time variable (instead of the more natural ) is to avoid a conflict of notation in the several changes of variables we will soon have to make.

The Black-Scholes terminal value problem for the value of a European call option on a security with price at time is

with , as and

Note that this looks a little like the heat equation on the infinite interval in that it has a first derivative of the unknown with respect to time and the second derivative of the unknown with respect to the other (space) variable. On the other hand, notice:

We eliminate each objection with a suitable change of variables. The plan is to change variables to reduce the Black-Scholes terminal value problem to the heat equation, then to use the known solution of the heat equation to represent the solution, and finally change variables back. This is a standard solution technique in partial differential equations. All the transformations are standard, well-motivated, and well known.

First we take and , and we set

Remember, is the volatility, is the interest rate on a risk-free bond, and is the strike price. In the changes of variables above, the choice for reverses the sense of time, changing the problem from backward parabolic to forward parabolic. The choice for is a well-known transformation based on experience with the Euler equidimensional equation in differential equations. In addition, the variables have been carefully scaled so as to make the transformed equation expressed in dimensionless quantities. All of these techniques are standard and are covered in most courses and books on partial differential equations and applied mathematics.

Some extremely wise advice adapted from Stochastic Calculus and Financial Applications by J. Michael Steele, [?, page 186], is appropriate here.

“There is nothing particularly difficult about changing variables and transforming one equation to another, but there is an element of tedium and complexity that slows us down. There is no universal remedy for this molasses effect, but the calculations do seem to go more quickly if one follows a well-defined plan. If we know that satisfies an equation (like the Black-Scholes equation) we are guaranteed that we can make good use of the equation in the derivation of the equation for a new function defined in terms of the old if we write the old as a function of the new and write the new and as functions of the old and . This order of things puts everything in the direct line of fire of the chain rule; the partial derivatives , and are easy to compute and at the end, the original equation stands ready for immediate use.”

Following the advice, write

and

The first derivatives are

and

The second derivative is

The terminal condition is

but so .

Now substitute all of the derivatives into the Black-Scholes equation to obtain:

Now begin the simplification:

What remains is the rescaled, constant coefficient equation:

We have made considerable progress, because

In principle, we could now solve the equation directly.

Instead, we will simplify further by changing the dependent variable scale yet again, by

where and are yet to be determined. Using the product rule:

and

and

Put these into our constant coefficient partial differential equation, cancel the common factor of throughout and obtain:

Gather like terms:

Choose so that the coefficient is , and then choose so the coefficient is likewise . With this choice, the equation is reduced to

We need to transform the initial condition too. This transformation is

For future reference, we notice that this function is strictly positive when the argument is strictly positive, that is when , otherwise, for .

We are in the final stage since we are ready to apply the heat-equation solution representation formula:

However, first we want to make a change of variable in the integration, by taking , (and thereby ) so that the integration becomes:

We may as well only integrate over the domain where , that is for . On that domain, so we are down to:

Call the two integrals and respectively.

We will evaluate ( the one with the term) first. This is easy, completing the square in the exponent yields a standard, tabulated integral. The exponent is

Therefore

Now, change variables again on the integral, choosing so , and all we need to change are the limits of integration:

The integral can be represented in terms of the cumulative distribution function of a normal random variable, usually denoted . That is,

so

where . Note the use of the symmetry of the integral! The calculation of is identical, except that is replaced by throughout.

The solution of the transformed heat equation initial value problem is

where and

Now we must systematically unwind each of the changes of variables, from . First, . Notice how many of the exponentials neatly combine and cancel! Next put , and .

The final solution is the Black-Scholes formula for the value of a European call option at time with strike price , if the current time is and the underlying security price is , the risk-free interest rate is and the volatility is :

Usually one doesn’t see the solution as this full closed form solution. Most versions of the solution write intermediate steps in small pieces, and then present the solution as an algorithm putting the pieces together to obtain the final answer. Specifically, let

so that

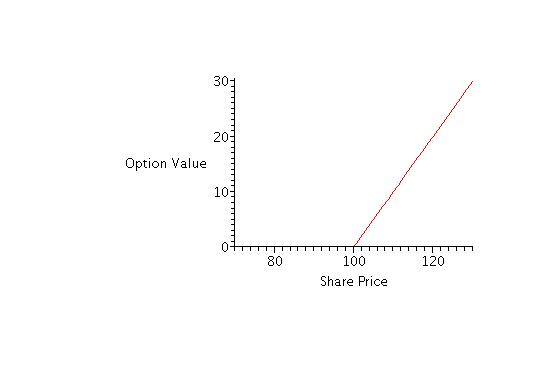

Consider for purposes of graphical illustration the value of a call option with strike price . The risk-free interest rate per year, continuously compounded is 12%, so , the time to expiration is measured in years, and the standard deviation per year on the return of the stock, or the volatility is . The value of the call option at maturity plotted over a range of stock prices surrounding the strike price is illustrated in 1

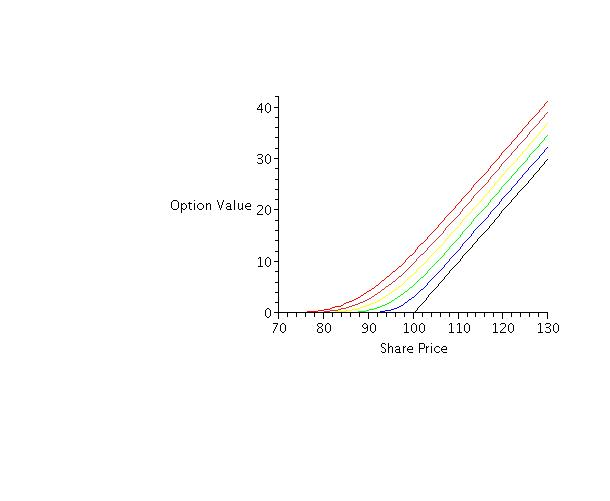

We use the Black-Scholes formula above to compute the value of the option prior to expiration. With the same parameters as above the value of the call option is plotted over a range of stock prices at time remaining to expiration (red), , (orange), (yellow), (green), (blue) and at expiration (black).

Using this graph notice two trends in the option value:

We predicted both trends from our intuitive analysis of options. The Black-Scholes option pricing formula makes the intuition precise.

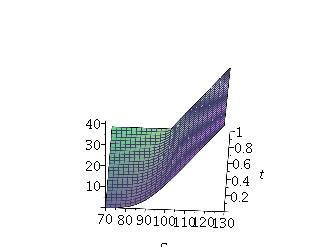

We can also plot the solution of the Black-Scholes equation as a function of security price and the time to expiration as value surface:

This value surface shows both trends.

This discussion is drawn from Section 4.2, pages 59–63; Section 4.3, pages 66–69; Section 5.3, pages 75–76; and Section 5.4, pages 77–81 of The Mathematics of Financial Derivatives: A Student Introduction by P. Wilmott, S. Howison, J. Dewynne, Cambridge University Press, Cambridge, 1995. Some ideas are also taken from Chapter 11 of Stochastic Calculus and Financial Applications by J. Michael Steele, Springer, New York, 2001.

_______________________________________________________________________________________________

__________________________________________________________________________

__________________________________________________________________________

__________________________________________________________________________

I check all the information on each page for correctness and typographical errors. Nevertheless, some errors may occur and I would be grateful if you would alert me to such errors. I make every reasonable effort to present current and accurate information for public use, however I do not guarantee the accuracy or timeliness of information on this website. Your use of the information from this website is strictly voluntary and at your risk.

I have checked the links to external sites for usefulness. Links to external websites are provided as a convenience. I do not endorse, control, monitor, or guarantee the information contained in any external website. I don’t guarantee that the links are active at all times. Use the links here with the same caution as you would all information on the Internet. This website reflects the thoughts, interests and opinions of its author. They do not explicitly represent official positions or policies of my employer.

Information on this website is subject to change without notice.

Steve Dunbar’s Home Page, http://www.math.unl.edu/~sdunbar1

Email to Steve Dunbar, sdunbar1 at unl dot edu

Last modified: Processed from LATEX source on February 5, 2012